The U.S. multifamily real estate market experienced dramatic shifts during the pandemic, with prolonged disruptions and atypical trends. Now, signs of stability are emerging, suggesting this sector may be regaining its footing.

Newmark reports record-setting demand in the second quarter of 2025, with steady absorption and declining vacancy rates — despite supply growth. However, rent growth remained flat for the second consecutive quarter, holding below 1%. These mixed signals point to deeper regional dynamics worth exploring. Let’s take a closer look.

Sun Belt:

The Sun Belt continues to lead in overall deal volume, with cities such as Dallas, Charlotte, Atlanta, Houston and Tampa driving activity. High renter demand is fueled by favorable climates, cost of living and business-friendly policies that attract remote workers.

Yet, rent growth has softened in many markets due to elevated construction and slower-than-expected absorption. Austin, for example, has seen a cumulative rent decline of 11.2% since 2023, followed by Phoenix (-6.5%), Orlando and Atlanta (both -4.1%) and Raleigh (-3.2%), according to Yardi Matrix.

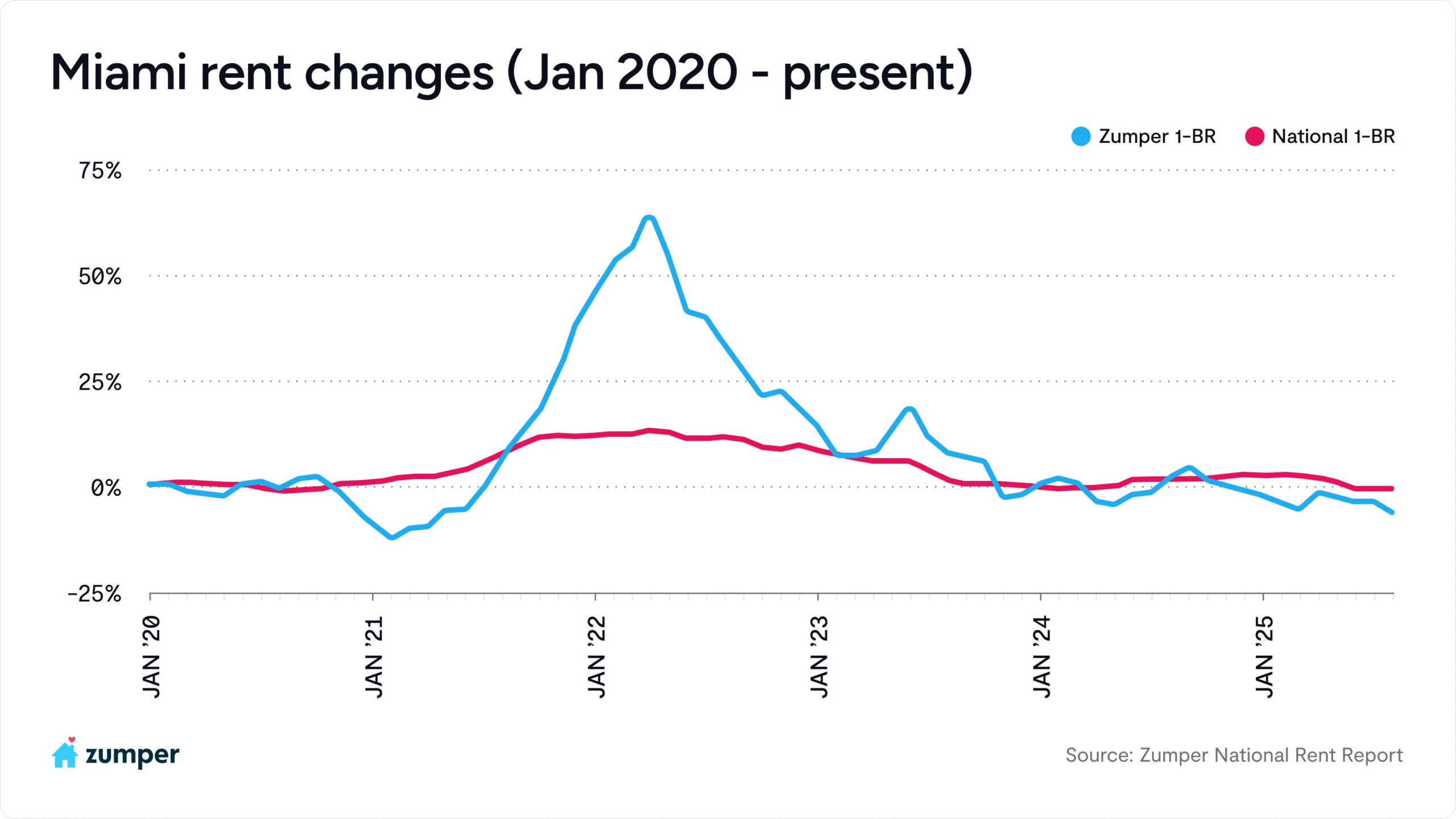

Miami, once a national leader in rent growth, is cooling due to oversupply and outbound migration. PODS ranks Miami third nationwide for move-outs in 2025. One- and two-bedroom rents are down 6.5% and 6.7%, according to Zumper, and with over 7,000 units permitted in the past year, rent growth is likely to remain subdued.

Phoenix saw the largest post-COVID vacancy rate increase in the region, driven by over 25,000 new units added in the past two years — accounting for 20% of Western U.S. completions, according to Kidder Mathews.

West Coast:

In contrast, West Coast markets such as Orange County, San Diego and Silicon Valley have experienced declining vacancy rates since 2019. Limited supply and high occupancy are driving rent growth and competition among renters, making these markets attractive to investors.

San Francisco posted the fastest annual rent growth among the top 10 markets in August, with one-bedroom rents up 8.2% and two-bedrooms surging 16.4% annually, according to Zumper. After years of pandemic-era declines, demand has rebounded as workers return to offices and new residents move in.

Meanwhile, Los Angeles ranked first nationwide for move-outs in 2025, according to PODS.

If we look at California, Oregon and Washington as a whole, rent growth has slowed. From 2021 to 2022, rents rose 21.4%, but growth in 2023 and 2024 totaled just 1.9%, reflecting a broader market recalibration, according to Kidder Mathews.

East Coast:

The New York MSA — encompassing northern New Jersey and Long Island — leads in loans originated since January 2024 and ranks first in property count and new units built since 2022, according to Cred IQ.

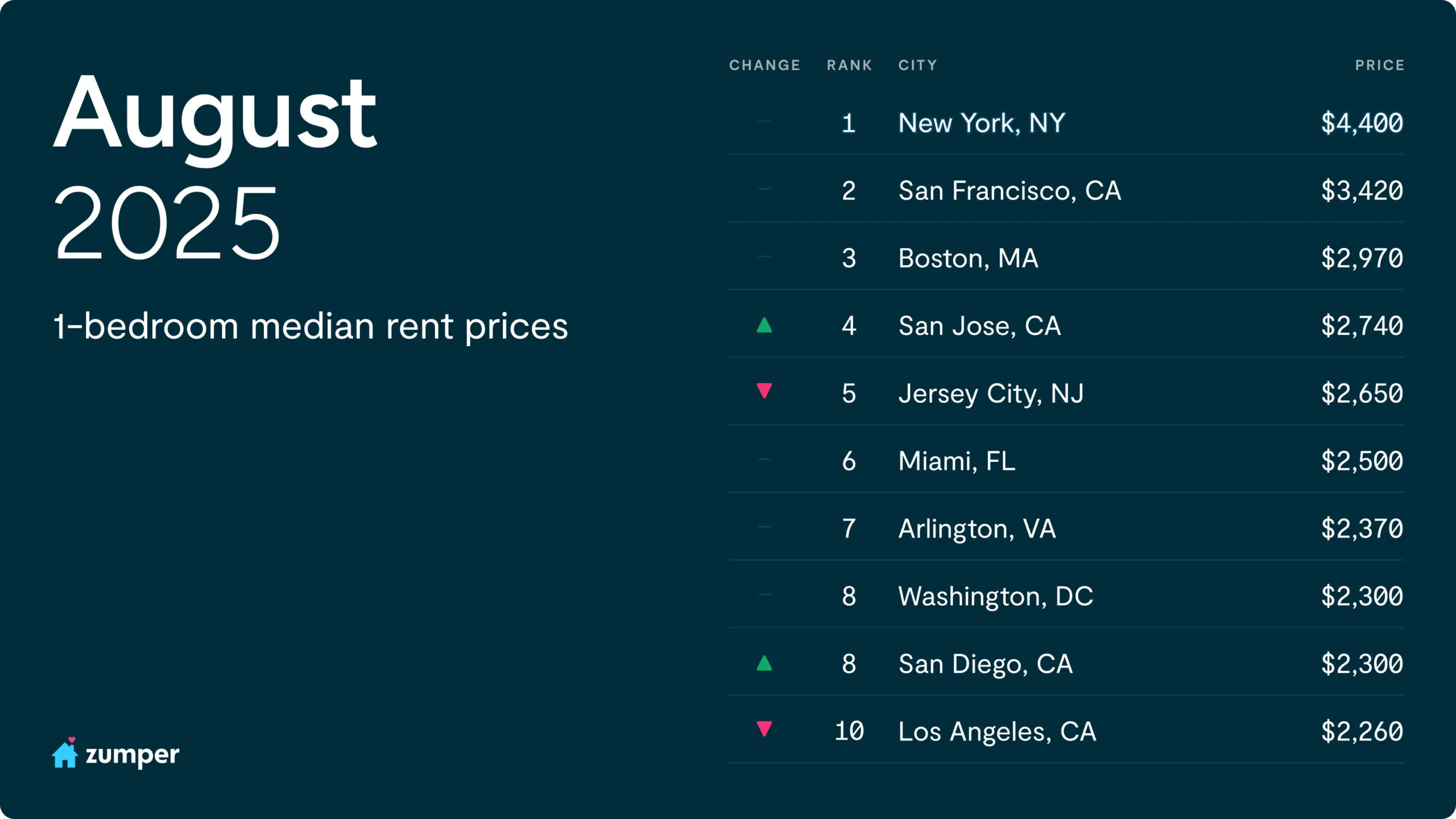

New York City remains the most expensive rental market in the U.S., with one-bedroom rents nearly $1,000 higher than second-place San Francisco, according to Zumper.

Washington, D.C., is also seeing steady demand, supported by limited supply, affordable rents and strong interest in affordable housing.

In contrast, Jersey City posted the steepest annual decline nationwide, with one- and two-bedroom rents down over 20%.

Midwest:

The Midwest shows strong fundamentals: rising rents, mostly declining vacancy rates and year-to-date sales up 35% compared to the same period in 2024, according to Northmarq.

Chicago and Kansas City led in rent growth, while Minneapolis-St. Paul dominated recent sales volume.

Vacancy rates rose in Indianapolis, Kansas City and Omaha, remained flat in Chicago, and declined in Cincinnati, Milwaukee and Minneapolis-St. Paul.

Construction activity has slowed, with first-half completions down 10% year-over-year period, driven by a 60% drop in Chicago. In contrast, Kansas City, Milwaukee and Omaha posted annual delivery increases of 50% to 80%.

Beyond region: Renting versus owning

High homeownership costs continue to keep prospective buyers in rental housing longer. Mortgage rates peaked at 7.8% in October 2023 and hovered in the low 6% range through mid-2025, making ownership unaffordable for many. The average mortgage payment is now 35% higher than the average multifamily rent, according to Kidder Mathews.

Newmark reports that renting remains significantly more cost-effective than buying, with the gap between the two widening well beyond historical norms. As of Q2 2025, the monthly cost difference reached $1,200 — three times the long-term average of $404. This sustained disparity is driving renter demand and strengthening the investment case for multifamily real estate.

As the U.S. MF market moves beyond pandemic-era volatility, signs of stabilization are emerging, but the recovery is far from uniform. Regional disparities in rent growth, vacancy rates and construction activity reveal a complex landscape shaped by economic factors, migration patterns and housing supply dynamics. For investors and stakeholders, understanding regional nuances is essential to navigating the evolving market in 2025 and beyond.