Following a year of increased transaction velocity and broader lender participation, the hospitality sector enters 2026 with stable occupancy and liquidity returning. At the same time, rising costs and uneven demand require investors to remain cautious as they weigh opportunity against policy‑driven risk, according to Marcus & Millichap. Inflationary pressures, labor constraints and elevated renovation costs are reshaping underwriting assumptions, influencing which deals close and rewarding disciplined execution in both acquisitions and financing.

Investment outlook: Activity Rises as Underwriting Tightens

Hotel transaction activity reached a three‑year high in 2025, driven by private investors, who accounted for three‑quarters of total sales volume. Institutional buyers made up most of the remaining activity.

Despite increased interest supported by easing interest rates and higher cap rates, buyers remain disciplined. Rising operating costs, labor shortages and demand uncertainty have led both private and institutional investors to maintain strict acquisition standards, with underwriting focused on the scope and cost of property improvement plans (PIPs).

Tariff‑driven inflation and labor shortages pushed renovation costs higher last year, creating friction in deal execution and narrowing the pool of viable transactions. Assets last renovated more than 10 years ago — about half of hotel trades in 2025 — face greater scrutiny, steering some investors toward recently renovated independent hotels not subject to brand‑mandated PIPs.

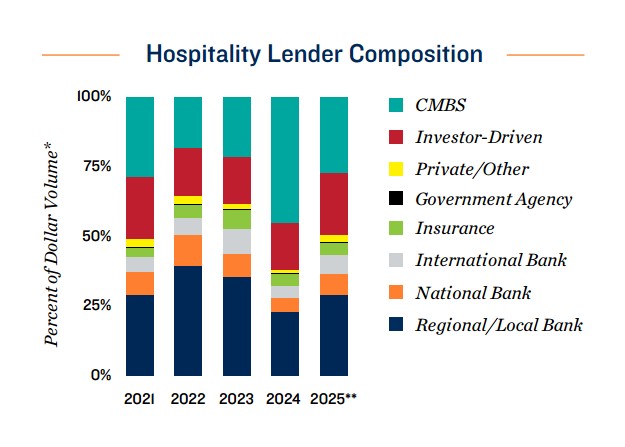

Capital Markets: Loan Maturities Drive Refinancing Activity

In 2025, local and regional banks, CMBS originators and investment funds were the most active lenders for hotel assets, each representing more than 20% of hotel lending volume, particularly in sub‑$5M to mid‑market transactions.

![]()

Upcoming loan maturities point to an active year for hospitality borrowers in 2026, especially for loans originated between 2019 and 2021. This is expected to drive refinancings, bridge extensions and recapitalizations rather than forced selling. Local banks remain the primary lenders for limited‑service hotels, while alternative lenders and institutional capital tend to focus on higher chain‑scale assets.

Hotel Fundamentals: Occupancy, Rates and Market Differences

Occupancy rates are stable but have slipped below prior cycle highs, placing pressure on revenue per available room, even as average daily rates continue to rise.

Full-service hotels, especially those catering to business travelers, have proven more durable than limited-service properties. Select‑ and full‑service properties recorded their first declines since 2020 last year, while limited‑service occupancy has declined for three consecutive years.

The middle to upper tier of the market remains better positioned to absorb future pressures, aided in part by a potential lift in consumer spending from anticipated tax refunds in 2026.

Constrained New Supply Brings Risk and Reward

Development headwinds continue to limit new hotel supply. Average daily rate growth has lagged CPI inflation, while tariffs have kept pressure on construction material costs and construction labor remains constrained due to a tightening labor market.

As a result, rooms under construction fell in December to their lowest level since 2018. This should support performance for existing assets, particularly in markets such as Las Vegas, San Francisco, Portland, Ore., Fort Lauderdale, Fla., and Minneapolis–St. Paul, where new supply is limited.

Macroeconomic Impacts on Hotel Demand

Tariffs, stricter immigration enforcement and geopolitical instability are weighing on economic growth, increasing inflation risk and intensifying staffing challenges for hotel operators. Estimates for 2025 suggest the U.S. experienced negative net migration for the first time in more than half a century. Slower migration has lowered the break-even level of job growth, tightening labor conditions overall, particularly within the hospitality sector. This places upward pressure on wages and operating costs.

The FIFA World Cup is expected to drive incremental demand in host markets. A 10% decline in the U.S. dollar last year could support international travel, though a $250 per‑applicant visa integrity fee will apply to many non‑immigrant visa seekers. While most Canadian and EU travelers are exempt, sentiment toward U.S. trade and foreign policy may still affect inbound travel.

Looking Ahead: Discipline Defines Returns in 2026

While fundamentals remain uneven, the investment landscape for hospitality real estate is becoming more defined, with 2026 shaping up as a year of recalibration rather than expansion. Capital is available, lenders are engaged and buyers are active, but execution risk remains elevated. Limited new supply supports existing properties, while higher costs and tighter underwriting require sharper asset selection and more deliberate financing structures. In this environment, disciplined strategies — rather than momentum — will drive pricing, deal volume and returns.