After a year defined by volatility, the 2026 commercial real estate outlook signals renewed confidence and opportunities.

Pricing and cap rates

As of October, capitalization rates on closed transactions rose 80 basis points from 2022 levels, suggesting higher potential returns for investors, according to Marcus & Millichap. This reset in pricing is attracting investors who are acquiring high-quality assets below replacement cost, adding well-priced properties with growth potential to their portfolios.

Interest rates and deregulation

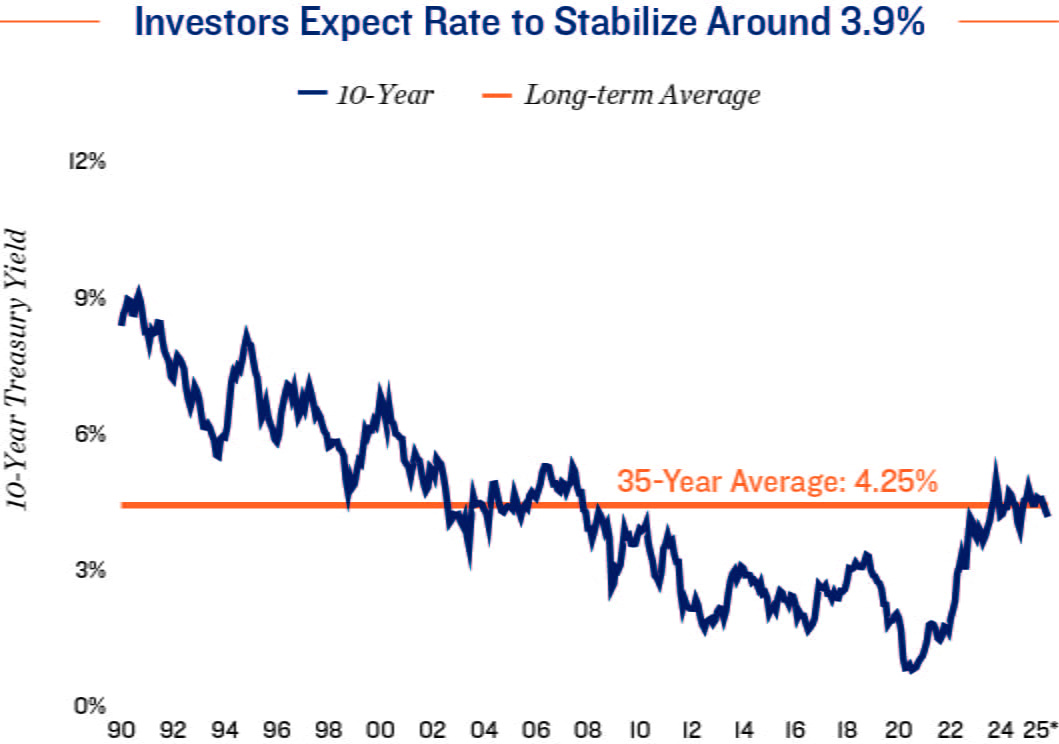

Investors expect the 10-year Treasury rate to stabilize near 3.9% next year, down slightly from 4.0%-4.3% in 2025, Marcus & Millichap reports. A lower rate means reduced borrowing costs, higher valuations and is a signal of economic stability.

Potential deregulation could also improve lending conditions by easing rules that limit loan availability. Looser regulations would allow lenders to provide more financing, giving investors easier access to debt capital for acquisitions and development.

GDP and inflation

The Blue Chip consensus forecast, based on 44 economists, projects GDP growth of 1.8% in 2026. If GDP is growing, the economy is expanding, and few economists expect a decline, according to Marcus & Millichap.

Inflation is expected to hold near 3% year-over-year. Stable Consumer Price Index (CPI) suggests economic steadiness. Most economists do not foresee extended inflation risk or a recession — positive signs for the market.

Unemployment and labor

The Blue Chip consensus forecast predicts a flat unemployment rate in the mid-4% range through 2026.

U.S. immigration has slowed, which means the labor force is growing more slowly, reducing monthly job creation needs from 75,000 in 2025 to 64,000 in 2026. Over a year, that is 750,000 new jobs needed to maintain the current unemployment rate, which is low compared to past years.

With slower labor growth and steady unemployment, wage and inflation pressures ease, making it more likely the Federal Reserve will hold or lower rates. That supports CRE demand by keeping borrowing costs manageable and boosting business confidence.

Equity trends

Investors anticipate near-term volatility in stocks, gold and other markets. If CRE enters a cycle of stability and growth, competition for CRE assets could rise, according to Marcus & Millichap. CRE offers predictable rental income and tends to retain or grow in value during inflation, making it a safe long-term play.

Sector-level opportunities

- Multifamily: Average rents remain below typical mortgage payments, keeping rentals attractive. Limited construction amid a housing shortage — estimated at four million to six million homes — adds support.

- Office: Positive net absorption since 2024 signals demand. High-amenity buildings in walkable urban cores are expected to outperform.

- Industrial: Small-bay and infill properties show strength. Slowing construction benefits existing assets.

- Retail: Stores anchored by or near a grocer or other necessity retailer generate the most optimism. A limited development pipeline adds stability.

Conclusion

Forecasts point to normalization for CRE, but outcomes hinge on tariffs, immigration policy and employment trends. Marcus & Millichap advises investors to monitor trade policy, target markets with strong demographics and job growth, leverage stable financing for acquisitions and consider value-add strategies in supply-constrained sectors.