A recent CBRE survey — based on 3,600 capitalization rate estimates from over 200 real estate professionals across 50 markets — indicates a trend toward stabilization in cap rates across most commercial real estate sectors, despite ongoing economic uncertainty and subdued expectations for sales volume in the first half of 2025.

The economic backdrop shifted briefly following the announcement of higher-than-expected tariffs on April 2. Markets reacted swiftly: stocks were sold off, treasury yields dropped and Moody’s downgraded the U.S. credit rating.

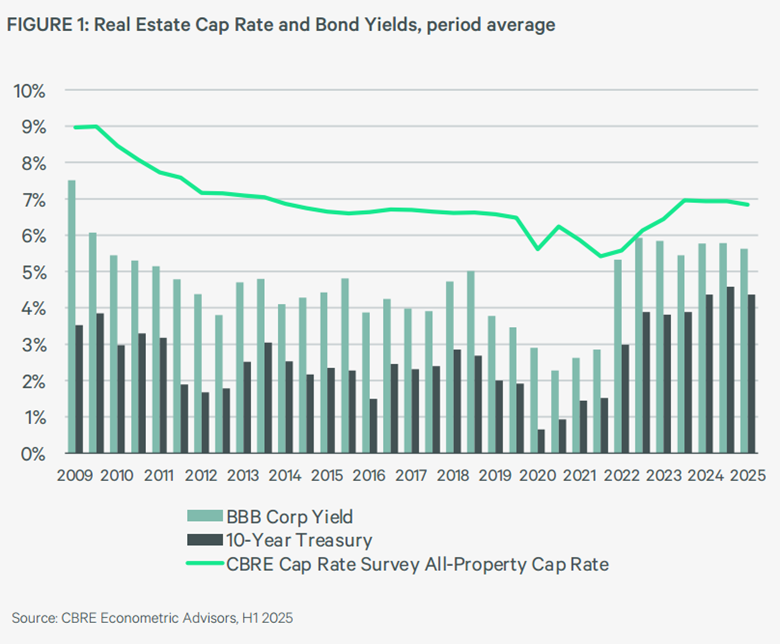

As a result, the 10-year yield rose to 4.8% mid-January before declining to 4.2% by the end of June, after the tariffs were paused.

Despite the volatility, the all-property cap rate estimate declined by nine basis points across most asset types, suggesting a move toward greater stability.

When asked about expectations for the next six months, most respondents predicted “no change,” while about a quarter of retail, industrial and hotel professionals said cap rates have peaked and will begin to decline.

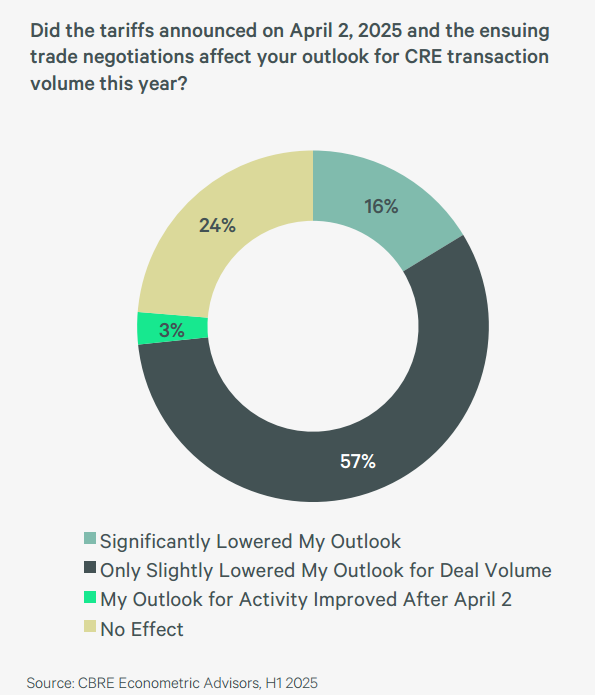

At the same time, economic uncertainties surrounding tariffs have negatively impacted the outlook for total sales volume in 2025. Over half of respondents anticipate slightly lower volume, 16% expect significantly reduced volume and 24% foresee no change.

Looking ahead, respondents predict multifamily assets will outperform other sectors in the long term, overtaking industrial properties. Retail is expected to remain steady, while the office sector will continue to face pricing uncertainty and wider valuation spreads.